Shifting Our Focus

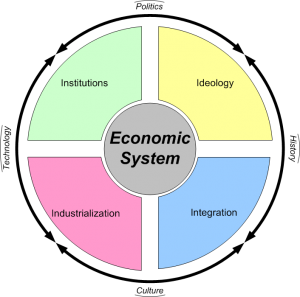

Although economic growth and increases in living standards have happened throughout human history, the really dramatic changes, the growth that truly transformed human life, doubled life expectancy, and made our modern world is a result of industrialization. It is the consequence of the industrial revolution (for our purposes, we can include the mechanized agricultural revolution as part of the industrial revolution). This industrial revolution is the consequence of changes in culture and technology. In Northern and Western Europe, a unique mix of change in culture (Renaissance, Reformation, and the Enlightenment) combined with discovery of new technology to trigger a revolution in how work was done, how goods were produced, and how economic activity was organized. In our model, think of a unique mix of the outside forces Technology and Culture triggering a revolution in the lower right corner, the “Industrialization” aspect of the economy (the red corner). Other countries in history had new technologies, and other countries had receptive cultures, but the right spark, the right combination happened in Northern and Western Europe.

The so-called “first world”, the United States, Canada, United Kingdom, France, Germany, Italy, Japan, Australia, and most all of Western and Northern Europe, experienced the Industrial Revolution first. In the last unit, we saw that the story of these nations in the 20th and early 21st century was largely about struggles over ideology. The reason ideology was the focus of these nations in the 20th century can be understood from our model. Essentially, (think back to your readings in Maddison), these nations had already struggled with and experienced rapid industrialization, a revolution in the red part of the model, before the 20th century. So the Industrial Revolution starts in the lower left (red) corner of the model, but the revolution, the change, spreads. Soon an Industrial Revolution, a revolution in how goods are produced and economic activity is organized, necessitates revolutionary changes in both Institutions and Integration.

The so-called “first world”, the United States, Canada, United Kingdom, France, Germany, Italy, Japan, Australia, and most all of Western and Northern Europe, experienced the Industrial Revolution first. In the last unit, we saw that the story of these nations in the 20th and early 21st century was largely about struggles over ideology. The reason ideology was the focus of these nations in the 20th century can be understood from our model. Essentially, (think back to your readings in Maddison), these nations had already struggled with and experienced rapid industrialization, a revolution in the red part of the model, before the 20th century. So the Industrial Revolution starts in the lower left (red) corner of the model, but the revolution, the change, spreads. Soon an Industrial Revolution, a revolution in how goods are produced and economic activity is organized, necessitates revolutionary changes in both Institutions and Integration.

Let’s briefly look at the kinds of institutional and integration changes that came about in these “first world” countries during this period. New institutions developed. Not only were corporations and large companies organized, but the very concept of a “corporation” as some distinct legal entity was created. Governance and the objectives of the government changed. All of these “first world” nations experienced a revolution in government during this period, some more than one. The US, Canada, and Australia were created from former colonies. Japan and western Europe experienced political revolutions and changes in regimes (not all were violent). Absolute monarchy gave way to elected governments. Even Britain, arguably the most stable and least revolutionary of theses countries, transformed from a monarchy ruling with the sanction of a land-owning class to a limited monarchy led by a popularly elected parliament in less than a century. Banks, paper money, contract law, stock exchanges, and civil courts for economic disputes all developed, indeed were created, in parallel with the industrial revolution. Eventually the combination of increasing industrialization and more complex financial systems created capitalism in the mid-1800’s.

At the same time as these Industrial and Political-Institutional revolutions were happening, these same “first world” nations were pushing for more trade, more resources, and expanded markets. They developed global empires. They began to economically integrate different parts of the world. Gradually, each country became less and less of a completely independent, stand-alone economy, and more of a piece of a larger global economy. Trade grew in importance. Very little of this increased integration was planned, just like the changes in institutions were not really planned. Change, particularly political and institutional change, happens as a result of responses to immediate crises. Rarely is it the result of design or plan. Indeed, the Communist Revolution in Russia is 1917 is notable for being one of the very few attempts at planned change. As industrialization grew and developed in the soon-to-be “first world” countries, so did the need for greater trade and integration. Originally, such trade was seen in terms of “empire”: a parent nation would expand its economy to include exclusive access to various colonies and conquered or subjugated lands.

So in terms of our model, the “first world” countries were experiencing more than a century of rapid changes, originally in industrialization, but soon also in institutions and integration. Most of the change was haphazard, unplanned, and unpredictable. The changes brought many very desirable outcomes: better living standards, wealth, increased democracy, more widespread literacy and education, longer lifespans, lessened power of monarchs and tyrants, new products, and new opportunities. But the changes also brought fearful, undesirable and poorly understood phenomena: urban poverty, unemployment, periodic financial crises, uncertainty, horrific total warfare, and a new powerful class of people called capitalists. By the early 20th century, constant change in industry, institutions, and integration appeared to be normal. Change was considered “normal”. But the path was not clear. It wasn’t clear where all these changes were leading. Was it progress leading to utopia? Or was it the road to doom and destruction for the average person? It was clear the role of government had changed. Government was now clearly supposed to be the representative of “the people” (20th century idea) and no longer “God’s representative on earth” (the 18th century view). But it was unclear exactly what that meant. By 1914, the revolution had spread from industrialization through institutions and integration and now converged on the issue of ideology. Essentially, it was time for the first world nations in the 20th century to try to make sense of the changes that had been happening to them. The conflicts, arguments, and focus was on ideology: What should the economic system be like? What should the government’s role be? What should the institutions be? In other words, industrialized nations spent the 20th century not only growing, but also fighting (often violently) about just what is the most effective, most desirable economic system.

Of course, the simplistic explanation of the 20th century claimed there were only two competing ideologies: communism/socialism vs. capitalism. In fact, there were (and are) many gradations and variations. There’s concentrated, privately owned but publicly directed capitalism such as characterized Nazi Germany and Fascist Italy. There’s centrally planned, government ownership of means of production Communism of the old Soviet Union (post 1928). There’s the social welfare state, government ownership of big industries but with market competition of mid-century Britain. There’s the monopolistic competition with the US with more or less Keynesian management of macro conditions. Even in the U.S., the economic system was significantly different between say 1948-1980 and 1980-to-present. Nonetheless, people began to group countries into 3 categories: first, second, and third worlds. The “first world”, of course, was the industrialized countries that we have been discussing. What these countries had in common was that they were heavily industrialized (generally) and had some variation of an economy with markets and capitalism in it. The “second world” consisted of the Communist (or at least USSR-aligned) countries. Sometimes the “second world” was industrialized (think Russia, Poland, Hungary), sometimes not. Usually, though, if countries in the “second world” were industrialized, they had come to it by a different history or path than Northern/Western Europe or Japan had.

End of the 20th Century: The First World, Capitalism, and Markets Win (or do they?)

During the “golden age” of 1950-1973, it appeared that the clear winner was a heavily Keynesian-managed, capitalist economy featuring competitive markets but with a social-safety net and a regulated banking sector. The centrally planned model of the USSR appeared to be an alternative based upon the rapid growth and industrialization it produced in the mid-century. But by the 1980’s, the scene was changing. Intellectually, the western “first world” countries came under the influence of an intellectual revolution that promoted a vision of unregulated “free” markets and unfettered big-business capitalism producing widespread wealth and freedom for all. Keynesian macroeconomic management, banking regulation, enforcement of laws promoting competition (anti-trust laws), and market regulation declined.

The more significant change happened in the so-called “second world”. Remember that before the 1980’s, the term “second world” was just another word for the “communist bloc”: the communist countries aligned with the Soviet Union. But by 1980 cracks in the communist “bloc” were showing. Growth had stagnated in the USSR and throughout the Communist world. China had politically split from the Soviet Union in the 1970’s and in 1978 began to open itself to market reforms. By the early 1980’s a political-economic revolution had started with a labor union in Poland’s shipyards that would eventually topple communism in central-eastern Europe. By 1989 the Berlin Wall was torn down. By 1991, the USSR itself imploded. Except for Cuba and North Korea, the Communist world had disappeared.

Intellectually, it appeared that the questions of “ideology” were settled. One popular political historian even published a book titled “The End of History” based on the idea that conflict over how economic-political systems should be organized was now settled for good. It appeared that “deregulated, free-market, free-trade capitalism” – what most people outside the U.S. call neo-liberalism – had won the battle of ideologies. Discussions of “economic systems” shifted. No longer was ideology the topic. By the 1990’s, world leaders didn’t talk about ideology so much. Instead, the topics became industrialization, “globalization”, and development. What had once been called the “second world” now became “emerging or developing markets”.

Instead of the second grouping of countries being defined as those with a communist system, it became those countries that were neither poor/underdeveloped nor fully developed/industrialized economies. New terminology emerged. These countries were called “emerging or developing markets”. Most all of the nations that had been communist (or their successors) are in this group: Russia, Poland, Hungary, Romania, China. But as this grouping of “emerging market” economies has grown to include others also. It now includes, Brazil, India, Turkey, South Africa, and others. These are countries that are at least partly industrialized, often growing rapidly, and clearly have the potential to someday become “fully developed” and join the “first world”.

Issues of Emerging Markets

“Emerging market nations” face many challenges, but they also have some advantages. Let’s look first at the advantages and then the major challenges.

Advantages

- Any of the “emerging market nations” have the advantage of being a “follower” when it comes to industrialization. They can copy existing technology. The how-to’s of how to create or operate a large industry have already been discovered and implemented in the older, more developed nations. This is particularly important when it comes to technology and factories. Consider the steel industry. In the U.S., Britain, and Germany, the steel industry developed over many decades, even a century. The processes and technologies used had to be invented (cost of R&D), tested, experimented, and finally through a process of marketplace competition, a winner selected. This process is long and costly. It results in much wasted investment (consider the factories built with technologies that didn’t work out). Present-day emerging nations, however, have the advantage of selecting the best already proven technologies based on the experience of the developed nations. It means growth and development can proceed faster because the best technology can be copied. It’s kind of like taking the freeway for your first journey to “rich-ville”. You get there much faster than the pioneers who had to first blaze the trails, cut the trees, pave the roads, and build the freeway in the first place.

- Low labor costs allow a starting point. Most (not all) “emerging market nations” have large populations able and willing to work (at present) for low wages. This allows the “emerging market nation” to focus initially on labor-intensive industries such as clothes-making, small consumer items, and electronics-assembly. The wage rate is often so low that it allows them to compete favorably against high-wage producers in developed countries, even when those high-wage producers have a productivity advantage from capital investment. It should be noted that this low-wage strategy only works in the early stages. As the “emerging market nation” grows itself and becomes richer, wages will rise and it will eventually be undercut by other poorer nations. Thus, Japan of the 1950’s was undercut by South Korea/Taiwan in the 1970’s which was undercut by China in the 1990’s-2000’s, who will no doubt be undercut by somebody in the future. The low-wage, labor-intense strategy does allow a start on industrialization. It also provides a nation with the beginnings of the institutions and experience necessary for more complex and sophisticated industries and technologies later.

- The ideologies of the developed world facilitate investment and trade, particularly the free-markets/financial capitalism/global business paradigm. By agreeing to the terms of the GATT/ WTO treaties, a country can gain access to broad export markets in the developed nations. Often the corporations of the developed world will facilitate and promote the nation’s development. (think Wal-Mart and China). Indeed, global corporations and banks from the “first world” are so eager to be part of these potentially huge markets, they bring large amounts of capital, knowledge, expertise, and technology. When the “first world” was industrializing, it wasn’t always so easy to cross-borders.

- A core of highly educated engineers, scientists, managers, and leaders is often available. China has always had a core of highly educated leaders at its helm. It is an ancient civilization. One benefit for India of their history as Britain’s colony (there were many disadvantages, too), is a high proportion of English-speakers and English educated leaders. English has become the lingua franca of the global economic community, so it has facilitated India’s growth in technology-based services such as computer programming. Russia, of course, had a very large number of highly educated scientists and engineers, dating back to the USSR

Challenges

- Large poor populations demand and require large resources, too. This is particularly true when the poor population is rural and based on subsistence agriculture or mining. These populations must be fed, housed, provided medical care, educated, and moved to urban areas to support an industrial economy. This has been a major challenge for Brazil, India, China, and Mexico.

- Geography. Historically, it has been easiest to grow, industrialize, and trade if your nation was on an ocean with numerous ports (preferably the North Atlantic), located in a temperate zone (the evidence is clear, but its not clear why this is so), and located with many neighbors who were also either rich or growing fast like yourself. Historically, if your nation was in the tropics, or land-locked, or on the Pacific or Indian oceans, or just in the Southern Hemisphere, your chances of growing industrially were low. Obviously a nation can’t move itself or change it’s geography (although heaven knows Imperial Russia tried for centuries to conquer and annex a warm-weather port!). It has to develop a strategy to overcome the limitations. Fortunately for today’s “emerging market nations”, technology in the form of air travel, the Internet, and electronic communications is helping.

- Demographics. Getting the right size and age of the population is important to industrialization, but for obvious reasons, very difficult to manage. If the population is too young, then there will be a huge need and demand for unskilled jobs – a potential resource for a low-wage strategy. But a large population (especially a growing one) can also mean too many mouths to feed. This could require devoting more resource to food and less to industry (it could be more labor for farming, or more $$ to purchase import food instead of machinery). But at the other end, too few people is an obvious disadvantage and having too old of a population is too. Currently, Russia is struggling with a very low birth rate (as is Japan and much of Northern Europe). These countries also face populations that are sharply aging. A major challenge in coming years for Russia will be finding enough workers. Interestingly enough, this could also prove a challenge for China in another 20 years. China implemented a strict one-child per family policy in the late 1970’s. Prior to then, it had very rapid population growth. Well the people born during the population boom years are now prime-age workers – the work force that is fueling their growth. But in another 10-20 years, they will start retiring. Then, the low-population rate since 1980 will mean a possible shortage of workers. Granted it is difficult to think of shortage of workers in a nation of 1.2 trillion people, but supply and demand is relative.

- Legal institutions. One of the greatest challenges of the formerly communist nations has been the creation of institutions to support financial capitalism and markets. Centrally planned communist countries had little need for contract laws, civil courts to handle trade disputes, laws for corporations, banks, or even court records of who owns what property. These institutions have all had to be created, people have to learn them, and the people have to accept them as legitimate. Much the same is occurring in China. In many of the poorer and emerging market nations of Latin America, a major challenge is the lack of legal title to land. People whose families have lived on and farmed a particular piece of land for decades or even centuries don’t have legal title to the land. The titles simply don’t exist. Without proof of ownership, these people cannot borrow to invest to improve the land, increase productivity, and grow output. Growth gets stopped cold simply from a lack of legal records.

- Culture, customs, diversity, and religion. Although diversity can be an economic advantage, economic history also shows it is frequently a disadvantage. The reasons are complex, but essentially amount to political conflicts. When a nation is ethnically or religiously diverse, especially when those different groups are sharply opposed to each other, there is a great tendency for conflicts over distribution of income, wealth, and power to take center stage. To keep peace, income, resources, and assets may not be distributed optimally to achieve the fastest growth. In other words, sometimes arguments over how to slice the pie prevent efforts to grow the total pie. In other nations, deeply ingrained cultural attitudes affect the ability and direction of investment and growth. India and China make a particularly interesting and sharp contrast on this issue.

Transitions

Clearly as the lists of “emerging market nations” and the wide range of incomes show, this grouping of economies is a very large, very diverse group. For our purposes in studying economic systems, we need to look at what these nations both have in common and how they are different. Beyond the fact of having a mid-range of income per capita, what most characterizes these countries is transition and a growing industrial sector. Typically these economies are countries that are newly industrializing or are re-industrializing. This means they are making dramatic transitions in their economic system. To a large extent, this definition of “second world” includes the countries that were classified in the old definition of “Second world”: the formerly communist countries. Russia, Hungary, China, Ukraine, Romania, and the other formerly communist nations are part of the new “second world” or “emerging markets” because their incomes are lower than developed nations and they are making the transition from a communist system to a more market-oriented, free-trade, capitalist system. But the new grouping of the “second world” includes many other countries making different transitions. Some, such as some Latin American countries are making a transition from a stagnant, oppressive class-based system left over from colonialism and centuries of land-based oligarchy. Another country, the world’s second-largest in population, India, is making a transition from being a poor colonial possession of Britain to having attempted a bureaucratic socialism in the 1950-1960’s to an advanced technology market-oriented services economy. And then there’s the example of China, a case all its ow

Since the key to the “emerging markets” is that they are all making a major transition, let’s take a look at what types of transitions are being made. I should note that each country is unique and faces its own transition challenges.

|

Transition

|

Examples:

|

| Industrial Communist, Central Planning to Capitalist Markets |

Russia, Poland, Hungary, Romania, Slovakia, Czech Republic, other former USSR republics |

| Collective Agriculture & Natural Resource-based Communism to Markets & Trade |

Ukraine, Russia, China, Romania |

| Poor subsistence agriculture to urbanized industry |

China, India, Indonesia, Malaysia, Mexico, Thailand |

| Former colonial or government bureaucratic control to markets & competition |

India, South Africa, Turkey |

| Government mercantilist policies and dependence on natural resource exports to modern industry |

South Africa, Brazil, Argentina, Mexico, Saudi Arabia, Persian Gulf States |

| Former class-, race-, or land ownership- based oligarchy to popular governments & urban markets |

Brazil, Mexico, South Africa, Argentina, Venezuela, Columbia |

Role of Institutions, Integration, Culture, and History

Industrialization is the foundation of high incomes and wealth. After all, industrialization means that accumulated capital (machines, tools, factories, knowledge, technology) is applied to make labor dramatically more productive. In a poor economy, it is common to have most of the available labor devoted to just producing enough food for everybody. After industrialization, little labor is needed to feed everybody so that allows more labor to produce more income and the other goods we want. For example, in 2004, the average poor or undeveloped nation devoted 58% of its labor force solely to produce food to feed the population. Often that still wasn’t enough. Yet in the developed “first world” nations, only 3.2% of the labor force is needed to feed the population. In the U.S., each farmer produces enough food to (on average) to feed 99 people!. [source: http://earthtrends.wri.org/searchable_db/index.php?theme=8&variable_ID=205&action=select_countries – a wonderful research resource, check it out!]

It’s not possible to create an industrialized, rich economic system from scratch. All that can ever happen is to change an existing country’s system. That means starting with the existing history, politics, institutions, and culture. Each country has its own unique resources (or lack thereof) and its own degree of integration (trade) with the rest of the world. Each country has its own unique history of adoption of technology. There is rarely a shortage of leaders who want to either help another country to grow or to spark that growth within their own country. Unfortunately, most efforts at creating successful growth and development fail. One reason is that leaders often make the mistake of assuming there is one right path, or that what worked in another country will necessarily work the same way in a different country. These mistakes are compounded when leaders attempt to impose an ideology upon an economy as a “blueprint”.

| Example: When Lenin and the Bolsheviks took power in Russia in 1917, they took Marx’s (and Kautsky’s) descriptions of how a communist system would work as the “master plan”. However, Marx had envisioned communism as the end stage of an evolution of the highly industrialized capitalist economies. In effect, he envisioned that industrial capitalism would inevitably result in increasingly monopolization and financial crises. Eventually socialism and then later communism would be established by a revolt of the under-paid workers that would lead to workers jointly managing factories and production. Critical to this possibility was that the workers would already have experienced the industrial world, understood it, and would have the education, knowledge, and skills to manage. Marx was writing about how communism would work when it came to a nation like Great Britain with a long history of industrialization. But, instead of a revolution in an advanced industrial economy like Great Britain, the communist revolution happened in Russia in 1917. In 1917 Russia was still essentially a feudal agricultural nation. Russia was closer to the middle ages than it was to Great Britain in 1917. Yet, Lenin attempted to implement workers’ management syndicates (called “Soviets”) in the 1920’s as Marx had described. He attempted to impose a “blueprint” on a culture and institutions where it didn’t fit. The attempt failed. The culture, knowledge, institutions, and skills simply didn’t exist. Within a few years, what industries existed were failing and production dropping because the soviets lacked the skills necessary. Marx had envisioned worker syndicates “managing” enterprises in Great Britain. But in Britain even the lowest workers were literate and educated. Not so in Russia in 1917. By the late 1920’s the decentralized workers’ Soviets decision-making was replaced by centrally developed, government-imposed, military-like “5 year plans”. That worked. The workers’ culture and institutions at that time understood taking orders under threat. Of course, by the time Russians had a couple generations worth of experience in an industrialized economy (fast forward to 1980’s), they no longer were as responsive to threats and central directives. |

| More Examples: In another post we’ll look at the less-developed nations, the poor. Throughout the second-half of the 20th century there have been many efforts to help or industrialize these nations, often in the form of “aid”. Most of theses efforts have all failed miserably. Some efforts have actually made these nations poorer. What many “aid” programs have in common is that they are based on some ideology or pre-determined “blueprint” of what a nation needs to do to grow. |

Asian Tigers – Case Study in Adapting to Local Institutions/Culture

The collapse of the communist world, and with it the 3-part division of nations as free (1st), communist (2nd) or non-aligned (3rd), wasn’t the only prompt for a re-groupings of countries. In the period 1960-1990, four economies grew dramatically from very poor, undeveloped status to a very highly developed, high-income, industrialized status. These four were called the Asian Tigers: South Korea, Taiwan, Singapore, and Hong Kong. These four countries’ growth was notable not just because they grew so fast, but also because of the economic system/policies they pursued to do it. All four deviated in many ways from what was considered the “conventional wisdom” of the Western, developed nations. Each of these four sought to develop their own “path” based upon “Asian values” and not just the free-market capitalist ideology of the West. See the Wikipedia entry Asian Tigers for more explanation

The so-called “first world”, the United States, Canada, United Kingdom, France, Germany, Italy, Japan, Australia, and most all of Western and Northern Europe, experienced the Industrial Revolution first. In the last unit, we saw that the story of these nations in the 20th and early 21st century was largely about struggles over ideology. The reason ideology was the focus of these nations in the 20th century can be understood from our model. Essentially, (think back to your readings in Maddison), these nations had already struggled with and experienced rapid industrialization, a revolution in the red part of the model, before the 20th century. So the Industrial Revolution starts in the lower left (red) corner of the model, but the revolution, the change, spreads. Soon an Industrial Revolution, a revolution in how goods are produced and economic activity is organized, necessitates revolutionary changes in both Institutions and Integration.

The so-called “first world”, the United States, Canada, United Kingdom, France, Germany, Italy, Japan, Australia, and most all of Western and Northern Europe, experienced the Industrial Revolution first. In the last unit, we saw that the story of these nations in the 20th and early 21st century was largely about struggles over ideology. The reason ideology was the focus of these nations in the 20th century can be understood from our model. Essentially, (think back to your readings in Maddison), these nations had already struggled with and experienced rapid industrialization, a revolution in the red part of the model, before the 20th century. So the Industrial Revolution starts in the lower left (red) corner of the model, but the revolution, the change, spreads. Soon an Industrial Revolution, a revolution in how goods are produced and economic activity is organized, necessitates revolutionary changes in both Institutions and Integration.